The financial crisis of 2008 prompted a seismic shift in terms of how we look at banking. The systemic risks and limiting of competition became apparent, as we rethought traditional, concentrated-banking and its influence on the financial market. Over a decade later, efforts to increase competition and give the public more access to their financial data has amounted to a number of regulatory initiatives. One of the most recent and revolutionary changes is (you guessed it) Open Banking. We’re going to go through this new system of banking, its terminology, growths and the obstacles it has come across. More than that, we’ll introduce you to the Invatechs Open Banking app and show you how our wealth of knowledge is there to assist you.

HOW OPEN BANKING WORKS

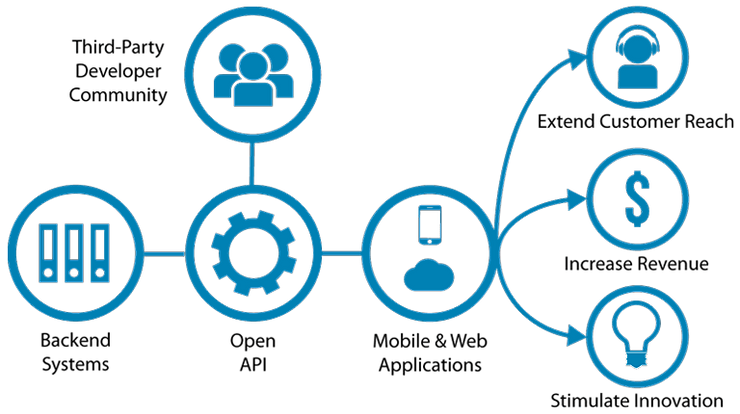

In simple terms, Open Banking gives you the opportunity to give your banking data to a third party, and aggregate your accounts into one place. From there, the data has the potential to allow companies to develop tailored products, apps and services you can use. This could be for things such as checking your credit score or monitoring your transactions and what you’re spending your money on. If you run a business, you could use Open Banking to give a third party access to your business bank account transactions which will offer you a host of benefits; we’ll get into those a bit later. It means you’ve got greater choice and transparency with your finances, whether it’s for your personal or business accounts.

In 2016 the Competitions and Market Authority published a report that found older and more established banks didn’t have to compete hard enough for customers and their business; this meant newer, smaller banks were finding it hard to access the market and grow themselves. With the introduction of Open Banking, the way we bank online has completely changed. With the introduction of PSD2 regulation by the EU, banks are required to give non-bank rivals access to customer payment accounts. PSD2 is an integral part of overseeing Open Banking compliance that you’ll come across a lot. The third-party providers are regulated, you can stop access to your data at any time, and you’ll have to verify their permission via your bank. All of this can be done through APIs (Application Programming Interface) with just a few taps on your phone. This makes Open Banking experiences secure, streamlined and designed to give you even more financial autonomy.

OPEN BANKING – TRENDS, GROWTHS AND RESEARCH

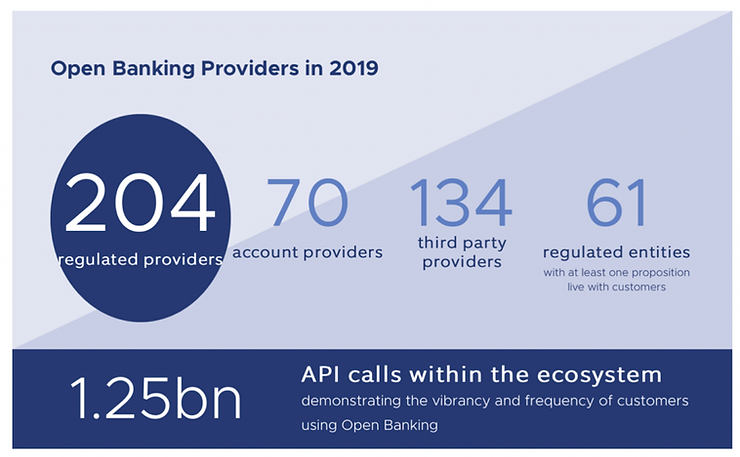

In such a short space of time, the effects and emergence of Open Banking have already yielded impressive results. Open Banking provided a review on its growth and influence in 2019. Open Banking in the UK for the first time surpassed one million users, and between June and December, the number of regulated providers grew from 104 to 204. Banks from NatWest to American Express and Metro Bank became a part of the Open Banking ecosystem, and by December of 2019, HSBC had signed a global partnership agreement to harness the power of Open Banking with the London-based FinTech start-up company called Bud.

Similar to the growth in automation, integrating technologies into companies’ infrastructure is key for their survival. Third-party aggregation-based companies and apps were some of the first Open Banking APIs that were launched, and they continue to evolve and provide more specific customer needs. But more than that, Open Banking is having a knock-on effect on the rest of the banking sector.

MasterCard delivered a report on providing ‘the promises of Open Banking’, concluding that Open Banking has the potential to bring the industry together, innovate and thrive through making more regulatory APIs available. As Open Banking was a response to the limitations of competition, putting the pressure on banks to develop and compete with their own PFM (Personal Finance Management) tools could lead to innovations in areas such as micro-saving, credit scoring as well as wealth management. On top of that, artificial intelligence has the potential to offer you relevant products, services as well as predict events in your accounts. In just two years since Open Banking has come to the market, mobile banking and automated technologies have innovated the way we deal with our finances, and as FinTech companies grow bigger and bigger in order to compete with traditional banks, you can bet the landscape will become even more innovative.

A SLOW START

Open Banking is still a new phenomenon, and with it comes some teething issues. The CMA9 as of the beginning of this year have struggled with achieving successful APIs calls, and banks and services providers still have some way to go with realising the full impact of PSD2. A lack of education on the PSD2 regulations, and a lack of infrastructure, has meant some banks have been slow on the uptake to incorporate Open Banking practises into their services. The German Federal Financial Supervisory Authority (or BaFin for short) initially allowed third party providers to maintain using non-PSD2-compliant old bank interfaces for clients and customers who are using credit card payments. But BaFin scrapped this loophole, and placed more requirements on banks to adapt and educate themselves on the regulations, after FinTech companies argued this didn’t sit within PSD2 guidelines and continued to push third party providers out. Even the UK which lead the way in Open Banking has to increase its number of PSD2-compliant gateways. As FinTechs lead the digital innovations in the market, traditional banks are at risk of falling behind the trend, and as PSD2 regulations have to be met, traditional banks have got more work to do if they’re to remain dominant in the world of banking.

HOW OPEN BANKING CAN HELP YOUR BUSINESS

It’s important you keep up to date with the evolution of Open Banking, certain growth trends, and certain obstacles. Nevertheless, there’s a wealth of ways Open Banking can help your business today. One of the main benefits of Open Banking is how it incorporates even more automation into your operations to cut down on cost and save you precious time. Lenders and accountants can pull the data they need via APIs, which means you won’t have to submit records and paperwork. Lending can be fast-tracked and streamlined, and automated accounting can track the payments you send and receive; this can also cut some of the costs for more expensive accounting processes. You might worry that as your bank account data becomes more widespread it's more susceptible to threats and breaches. However, PSD2 regulations set unified security standards, which means companies who fail to maintain security standards face harsh penalties, data can only be used for customers’ specific purposes, and practises such as screen scraping (that can be utilised as a means of fraud) are prohibited.

In basic terms, Open Banking gives you more transparency, control, saves you time and streamlines your services and operations. Now you’ve just got to find the service provider(s) right for you.

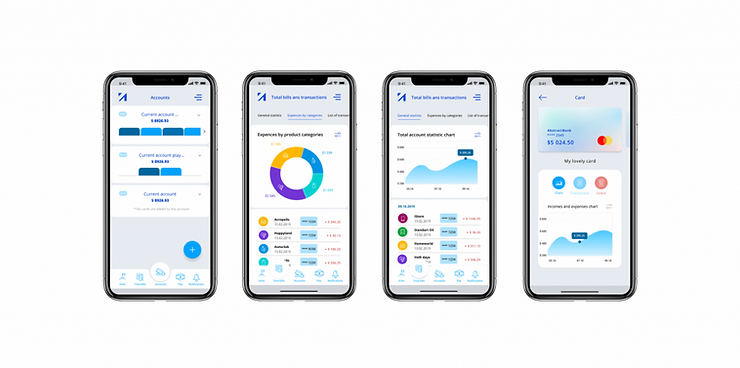

INVABANK

Invatechs provides a wide range of information and advice to help you with your digital needs. With our own Open Banking app InvaBank, we offer a highly customisable app you can apply to your business logic. You can view all your information on cards and accounts, account statements and transactions in one app. Our knowledge doesn’t stop there: our monthly portfolio updates cover topics from apps we’ve created to articles on money-saving advice. Get in contact with us today for a free demo and consultation - let us help you harness your digital potential.