The global economy is facing its deepest recession in eight decades in wake of the devastating impact of Covid-19. With the imposition of social distancing and self-isolating protocols, entertainment, travel, tourist, sport industries and more have had to shut down or drastically adapt to meet new conditions. Global Economic Prospects forecast a 5 percent contraction for the global economy in 2020 alone. Nevertheless, out of the damage Covid-19 has wrought comes the potential for new, innovative methods of using Digital Financial Services (otherwise known as DFS) as a means of short term and long-term sustainable recovery efforts. DFS and Fintech solutions were achieving growing international traction prior to Covid-19, but have had to scale up quickly as a result of the pandemic. Now more than ever is the time to embrace the potential of Digital Financial Services with better automation, open banking APIs and micro-credit platforms. In this article, we’re going to take a look at some of the illuminating research into DFS’ potential during Covid-19; particularly in the Global South. We’re also going to take a look at Invatechs’ own Digital Financial Services and the potential they could provide for you, your business and today’s global economy.

WHAT ARE DIGITAL FINANCIAL SERVICES?

Let’s start with the basics, what is a Digital Financial Service? DFS refers to financial services like payments, credit and remittances that are delivered through digital channels, like mobile devices. New solutions such as Peer-To-Peer (or P2P) lending, cloud computing, mobile payments, crypto-assets and more all fit under the DFS bracket as new innovations that have appeared in the last 10 years.

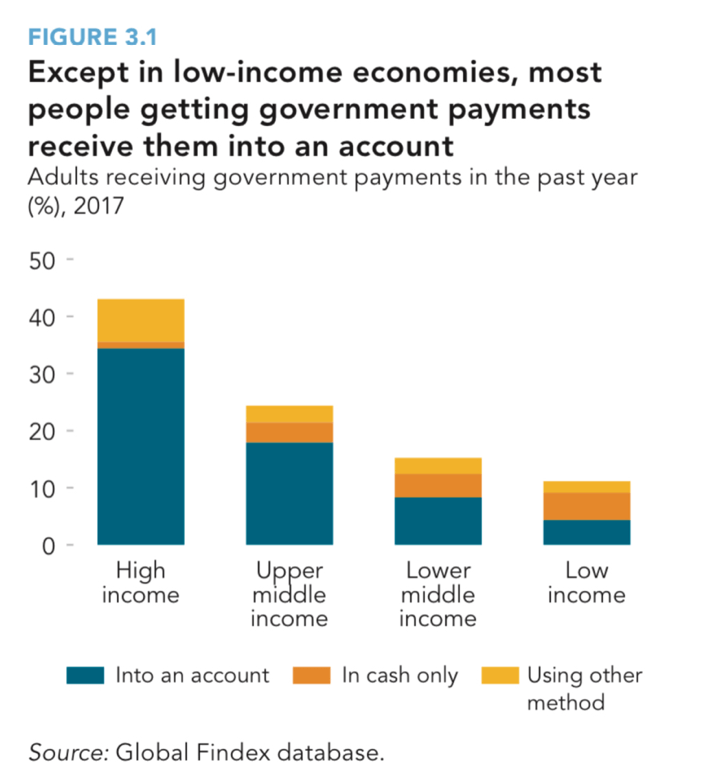

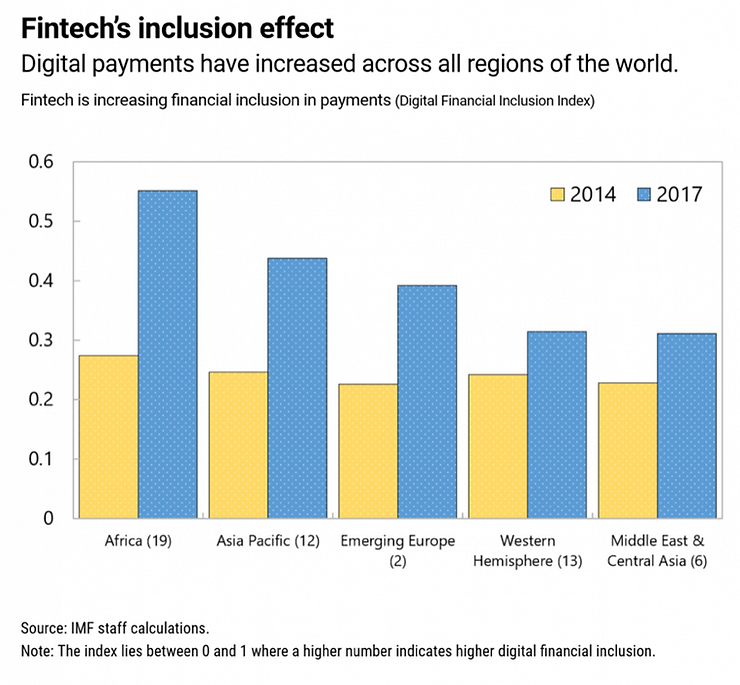

Governmental payouts (often referred to as G2P) particularly harness DFS: an automated text message alert can let you know that a pension, scholarship, tax refund and more has been paid into your account. In 2017, 16% of individuals received government transfers and payments digitally, and between 2014 – 2017 there was a global rise from 62% to 69% of people who use or access a financial service via a mobile money service. DFS’ potential has been very well harnessed in developed economic countries, as most individuals are likely to get a G2P payment or a G2B payment via a digital account.

Digital Financial Services now play a key role in our economy and tech’s economic ecosystems, but Covid-19 has shone a spotlight on them like never before, revealing how deeply necessary high-quality digital infrastructure is for accessible DFS for everyone. DFS can even play a role in slowing down the virus’s transmission and helping with social distancing, whilst committing to making the economy accessible to more and more people.

COPING DURING COVID – How Digital Financial Services are Being Used and Developed:

DFS provide secure, low-cost and contactless financial tools directly to your account, which has been particularly useful during the spread of Covid-19. Furlough schemes across Europe have meant non-essential workers have been able to stay at home which has incentivised the ability to self-isolate; simply put, DFS have fewer health risks than in-person cash-based relief. More than that, digital payments and transfers are more cost-effective according to the Better Than Cash Alliance. Above all, things like E-commerce payment systems allow for speedy transfers to targeted households and individuals, which is crucial for those in need of financial assistance right now.

With the development of Fintech (and if central banks issue digital currencies), there’s potential for governments to track spending data and see which sectors are in decline and in need of financial support. More complex data revealed through digital currencies allow for insights into transaction volumes and values; this of course will be dependent upon a country’s privacy laws. The scope of more digitised payments and transfers could also improve visibility for tax payments, evasion and corruption, which will be particularly useful for increasing tax revenue during Covid-19.

So we can see from the outset the potential DFS has right now for Covid-19 relief. Furthermore, there is even the case made in behavioural science for more digital financial inclusion through DFS; small ‘nudge theory’ tactics such as offering digital transactions at cash-out as well as offering the ability to pay for healthcare and financial services without visiting a branch could transform accessibility for places in the Global South (that are more dependent on in-contact meetings to access resources), whilst maintaining social distancing during Covid-19. Africa and Asia are leading the way, with countries such as Ghana, Kenya and Uganda as front runners for more digital inclusion with better digital payment services.

BUILDING FOR THE FUTURE DURING AND AFTER COVID-19:

Similar to the fast expansion of China’s digital payments and E-commerce in response to the SARS epidemic of 2003, DFS has accelerated internationally due to Covid-19. Research into Fintech solutions and DFS accessibility has also unearthed revealing information surrounding the gender pay gap and women’s accessibility to DFS in low and middle-income countries. Accessibility to a phone wields huge potential for women’s accessibility to better finances.

However, investment and expansion of digital infrastructure play a key role in unlocking DFS’ potential; this includes better digital identification as well as biometric systems, open APIs, the correct legal and regulatory frameworks and better mobile broadband infrastructure. At Invatechs, our own expertise and continuous development in these fields offer solutions and potential for more accessible DFS and technology. Let’s look at some key areas as well as some of our own services and products.

Open Banking APIs:

We’re well aware of the power Open Banking puts into consumers’ hands, as it provides clear financial information as well as features for future investments, saving, transparency, spending reports and third party offers. For these reasons, it could become an invaluable financial tool for those economically disenfranchised, provide pathways for better-digitised transfers and spending, as well as better access to loans and savings. Beyond just this, the growing shift towards SMEs using Open Banking could be particularly attractive for Covid-19 recover as SMEs can access new products and compare accounts. In just the space of 2 years, Open Banking has produced more vendors and competitors as well as a growing uptake of Open Banking payments during Covid-19, due to increased social distancing and a growing preference for online shopping and purchasing methods. We’ve got an entire Invablogs article dedicated to the world of Open Banking and what it can offer we’d recommend checking out for a deeper dive into its potential.

Micro-Credit Platforms:

With such a sharp and sudden change to the world’s finances, more and more people have looked to micro-credit platforms, particularly low-income households and groups employed in the informal sector who are worst hit by the pandemic. Financial inclusion is paramount now more than ever. Fintechs responding to this increasing market will need the very best data science and analytics to risk mitigation from digital lending companies. Before the spread of Covid-19, attention was paid to the potential micro-credit has for providing easy capital to those who need it. At Invatechs, we created our own micro-credit platform and solution with Vance Pay that provides advanced payments through unearned income in exchange for a transaction fee. By simply texting the amount an employee needs to a VancePay number, they can get the money transferred into their accounts; proving particularly useful for when any unexpected financial needs come up, which is especially pressing during the Covid-19 pandemic. More than that, we have an entire blog post dedicated to creating your own Peer-To-Peer (or P2P) lending platform, another form of micro-credit that has grown in popularity in 2020. It’s important to note the rollout of micro-credit is dependent upon a country’s own laws and jurisdictions but could prove as an incredibly useful service for both businesses and the general public.

Data and Automation:

As more people become dependent on web channels, personalised data information, advanced AI and analytics will be a driving force for providing the best services and data strategy. Automation is vital now more than ever in the workplace, pre, during and post Covid-19. Automated payroll systems that could aggregate the correct furlough funds and working hours play a vital role in everyone’s financial health. The need for automated systems has become particularly prescient with more of the workforce going off sick; the need for customisable and automated payroll systems has been needed now more than ever to adapt to changing workforces. Other automated services such as chatbots and voice activation services have been used as a replacement for a smaller workforce, and QR codes have collected location-specific information about people to monitor the disease’s spread. Invatechs’ own payroll solutions ensure accurate and data-driven results with automated calculations that are fit for the scalable operations Covid-19 prompts in pay and government financial assistance – you can check out our cloud-based payroll software we designed for NHS GP practises to find out how we do it.

COVID-19, DFS and FINTECH POTENTIAL:

Despite the devastating impact Covid-19 has had on our economy and lives, the rapid turn around of DFS and Fintech solutions could mean a vast and fast expansion of financial accessibility. Internationally we have become dependent on DFS for our safety and social distancing, whilst countries find new solutions to develop digital infrastructure and create incentives through digitisation. Easy to use applications that tap into Open Banking, micro-credit and automated potential are crucial now and for post Coronavirus growth.

At Invatechs, we’re dedicated to creating products and solutions for financial challenges amongst many other areas. We have a blog post all about staff augmentation vs outsourcing that will be particularly useful for adapting to the changing demands of workforces during the pandemic. We continue to look for opportunities to develop products and services for companies whilst committing to using our own expertise that can help during the pandemic: whether that’s developing and using software and technology for micro-crediting, creating a payroll system that ensures your employees get the government relief they need or providing businesses and consumers with financial transparency through our Open Banking app, InvaBank.

If you’re looking to develop your own solution from the ground-up or with your existing systems or you just want to learn more about the potential DFS has to offer, don’t hesitate to contact us today.