Fintech Software Trends and Banking Apps in 2025

Fintech software is evolving rapidly. Maybe faster than most executives realize. In 2025, banking apps, payment APIs, and digital financial platforms aren’t just conveniences—they’re strategic tools for businesses, banks, and consumers alike.

If you’re a founder, CTO, or CFO, you’ve probably felt the pressure to stay ahead. And honestly, it’s challenging. Between compliance, customer expectations, and technology shifts, keeping up feels like a moving target. But understanding trends can save months, maybe years, of trial and error.

The fintech landscape isn’t about flashy features alone. It’s about solving real problems: speeding up transactions, increasing security, and making financial services accessible. If you’re exploring fintech software solutions, understanding the top trends in banking apps and payment APIs is essential for staying competitive. So, let’s dive into the top five fintech app development trends in 2025, with real-world examples and practical insights.

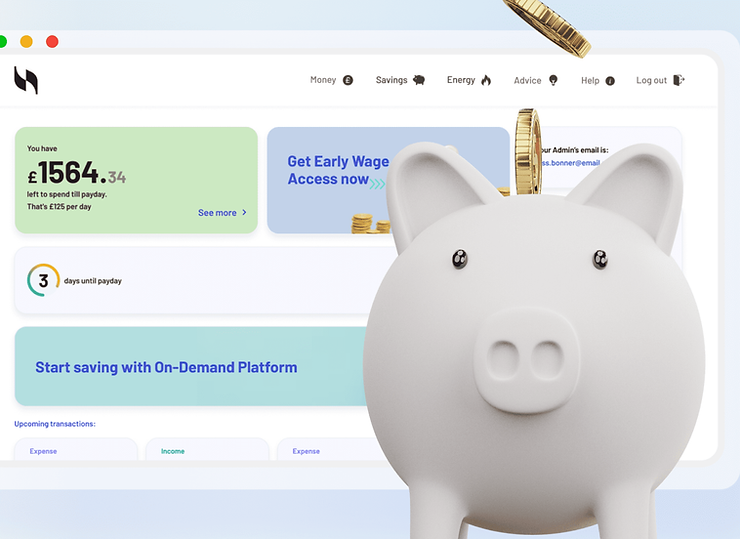

1. Embedded Finance and Banking-as-a-Service

Embedded finance continues to expand. In simple terms, it’s when non-financial platforms integrate financial services directly. Think retail apps letting customers pay, get credit, or manage money without leaving the platform.

Why it matters:

- Increases customer retention by keeping users inside your ecosystem.

- Opens new revenue streams without building a full banking infrastructure.

- Leverages payment APIs for seamless transactions.

Real-world examples:

- Some e-commerce apps offer installment payments at checkout. Conversion rates often jump 15–20%.

- Ride-hailing apps allow users to maintain wallet balances, pay for rides, or transfer funds directly.

Observation: I recently looked at an embedded finance demo, and the simplicity was striking. The platform enabled microloans in seconds without traditional bank friction. It made me wonder why more companies aren’t doing this yet.

Implementation tip: Start small. Add one financial feature first, then scale. Trying everything at once can overwhelm your team and your customers.

Book a free consultation to explore embedded finance integration for your platform.

2. AI and Machine Learning for Personalized Banking

AI isn’t hype anymore. Maybe it’s finally practical. Personalized banking apps can now suggest saving habits, flag unusual spending, and recommend investments.

Key applications:

- Fraud detection using ML algorithms.

- Personalized insights in real-time.

- Automated chat and voice assistants for customer support.

Scenario: One bank uses AI to alert users when spending patterns suggest a potential fraud attempt. Notifications go out within seconds, and customers confirm suspicious transactions before any real damage occurs.

However, privacy is tricky. Banks must balance personalization with compliance. HIPAA, GDPR, and PSD2 regulations require careful handling of personal data.

Observation: I’ve tested a banking app where AI predicted potential overdraft situations and suggested actions. It worked—but only because data was structured well. Many apps fail because raw data isn’t clean.

Contact an expert to see how AI can enhance your banking app.

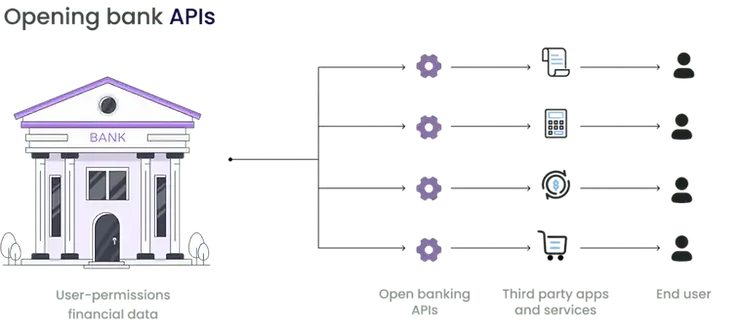

3. Open Banking and API Ecosystems

Open banking depends heavily on API integration for fintech platforms, enabling seamless account aggregation and third-party services. You might also consider developing custom APIs to connect legacy systems.

Benefits:

- Allows customers to manage multiple accounts in one app.

- Encourages fintech startups to innovate on top of traditional banks.

- Reduces development time through reusable APIs.

Real-world example: A fintech platform lets users view their checking, savings, and investment accounts across three banks in a single interface. It’s convenient, though sometimes inconsistent APIs can slow things down.

Personal note: I’ve seen several open banking integrations fail because of poor documentation. It’s a reminder: technical details matter as much as business vision.

Implementation tip: Partner with reliable banks and focus on API quality. Even minor inconsistencies can frustrate users.

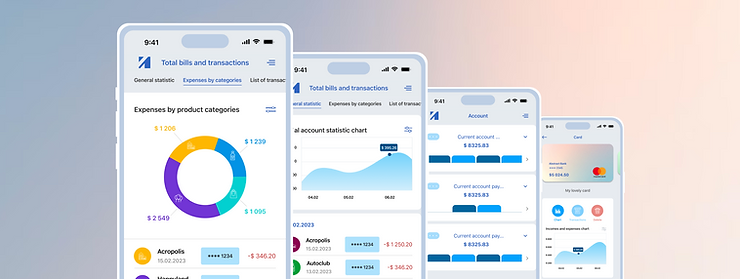

4. Mobile-First and Super Apps

Mobile-first fintech apps are evolving into super apps. They offer payments, banking, insurance, investments, and loyalty programs all in one.

Advantages:

- Customers prefer fewer apps.

- Streamlined UX improves engagement and retention.

- Easier integration with payment APIs and third-party services.

Example: In Asia, super apps combine bill payments, microloans, food delivery, and transportation. It works because the app keeps users inside a single ecosystem. Maybe Western markets will follow.

Tip: Start with core features—payments or account management—then expand. Overloading a new app can backfire.

Observation: I recall a demo where the super app concept was tested in a small city. Users loved it, but adoption stalled because too many features were introduced too quickly.

Many fintech super apps rely on a Node.js backend for fintech apps to handle high-volume transactions efficiently. Our team’s experience in Node.js development ensures scalable and secure platforms.

5. Enhanced Security and Regulatory Compliance

Fintech apps face growing scrutiny. Compliance with PSD2, GDPR, or local banking laws isn’t optional.

Trends:

- Biometric authentication (fingerprint, facial recognition).

- End-to-end encryption for data in transit.

- Continuous API monitoring for suspicious activity.

Scenario: A mobile banking app introduced facial recognition and instant fraud alerts. Trust increased, and users spent more confidently.

Observation: Security lapses kill trust faster than poor UX. I’ve seen apps with amazing features fail simply because users felt unsafe.

Implementation tip: Prioritize security early in development, not as an afterthought.

For enterprise applications, Java-based fintech platforms are often preferred due to stability and security. Choosing the right stack can make the difference in delivering enterprise-grade fintech software.

Top Fintech App Trends to Implement in Your Business

2025 is an exciting year for fintech software. Embedded finance, AI personalization, open banking APIs, mobile-first super apps, and security are the trends that truly matter. Staying ahead isn’t just about technology—it’s about aligning solutions with customer needs and regulatory realities.

Don’t wait. Book a free consultation today to explore how these trends can be applied to your fintech app. Or contact an expert to start designing your next banking or payment platform.