Credit Risk Scoring Is Broken—And It's Costing You

Loan brokers and lenders walk a tightrope every day:

- If you approve the wrong borrower, defaults rise.

- If you reject good borrowers, revenue stalls.

- And if you take too long to decide, clients go elsewhere.

The pressure to act fast—while staying compliant and accurate—is enormous. Yet many underwriting systems rely on outdated processes:

- PDF uploads and manual document parsing

- Static bureau scores that miss recent behavior

- Hardcoded scoring rules that don’t evolve

This results in high operational cost, inconsistent decision-making, and risk exposure.

There’s a better way.

At Invatechs, we build AI-powered lending platforms that handle risk scoring, fraud checks, and borrower profiling in seconds—not hours. We’ve helped UK and US brokers implement custom credit engines that improve speed, accuracy, and profitability.

Real-Life Challenges in Lending Platforms

From our work with loan broker platforms and invoice financing clients, we hear the same problems repeatedly:

- “Our underwriters are overwhelmed.” They sift through PDFs and spreadsheets manually.

- “We lack real visibility into borrower behavior.” Bureau scores don’t tell the whole story.

- “Our tech can’t scale.” Each new loan officer adds overhead, not efficiency.

For example, a digital lender processing 300+ deals per month was losing time manually reviewing each submission. Underwriters had no clear risk indicators beyond a basic credit score, and time-to-offer exceeded 24 hours for even standard cases.

This made them lose competitive deals—and onboard riskier borrowers due to lack of insight.

What AI Adds to Credit Risk Scoring

With an AI-powered scoring engine built by Invatechs, lenders can:

Automate risk evaluation in minutes using structured and unstructured data. Spot patterns human underwriters might miss (e.g., behavioral shifts, anomalies). Continuously learn from past lending outcomes and update thresholds in real-time.

Key Data Sources Used:

- Banking API data: cashflow, balances, income stability

- Open Banking feeds (UK): real-time transactions

- PDF parsing (OCR + NLP): contracts, invoices, IDs

- Business profile data: company age, industry trends

- Behavioral analytics: login frequency, changes during application

All this data is run through a machine learning model trained on past approval outcomes—fine-tuned to your unique policies and appetite.

Day-to-Day Workflow (Before vs After)

Before AI Integration:

- Manual checks for affordability, fraud, and compliance

- Credit score and internal checklist applied case-by-case

- Underwriters lose time, overlook key signals

After Invatechs Implementation:

- Application data is parsed instantly (including PDFs/images)

- Risk score and red flag report is auto-generated

- Offers are pre-structured based on profile, loan size, repayment ability

Result: Underwriters become decision-makers, not data entry clerks.

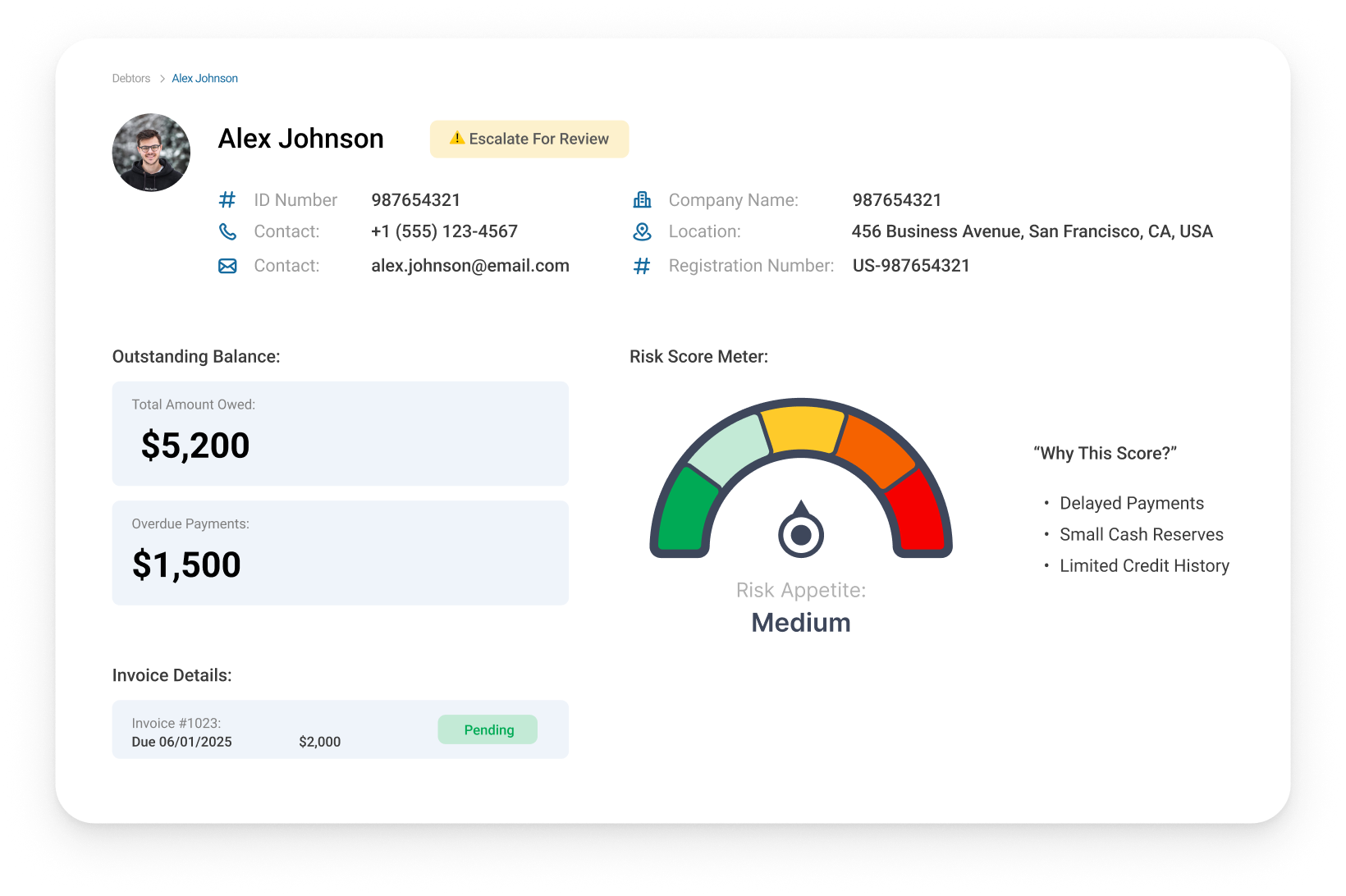

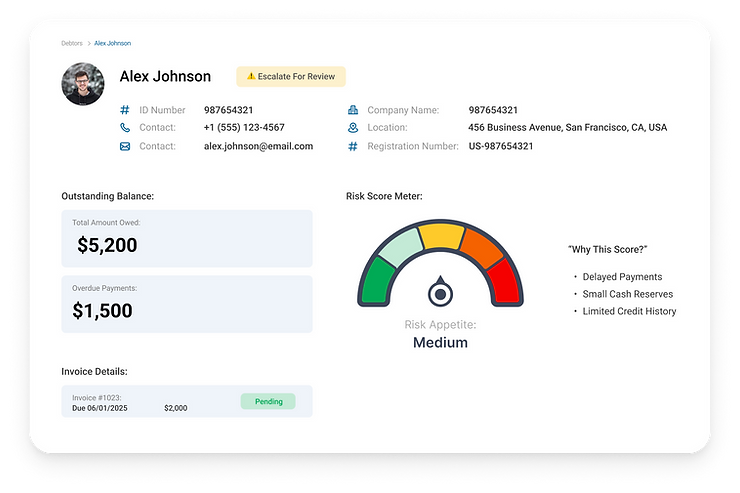

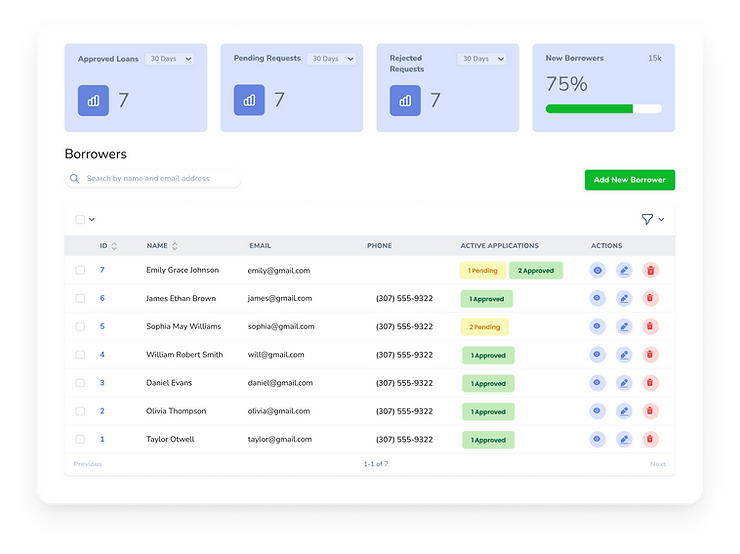

Real-Time Dashboard Example

Lenders receive:

- Borrower risk score (with rationale)

- Estimated default probability (based on similar profiles)

- Recommended deal structure: amount, term, interest rate

Borrowers see:

- Application status updates

- Required documents or missing data

- Offer timelines

This transparency improves both borrower experience and compliance audit readiness.

Architecture: How the Platform Is Built

Backend: Node.js handles API integration, scoring logic, and queue-based processing for real-time applications. Frontend: React or Vue.js for dashboards (borrower, lender, underwriter views). AI Models: Python-based ML engine using scikit-learn or TensorFlow. Hosted in AWS with CI/CD pipelines for model updates. Security: JWT/OAuth2, audit logs, document encryption (at rest + in transit). Storage: PostgreSQL + MongoDB for hybrid structured/unstructured data management.

This modular architecture allows you to:

- Add new data feeds as regulations evolve

- Retrain scoring models as your loan book grows

- Maintain speed and uptime as you scale to new regions

Business Impact Snapshot (Based on Real-World Results)

For a lender processing 400 applications/month:

- Time saved per application: 10–15 minutes

- Monthly underwriting cost saved: £3,000–£4,500

- Default rate drop (within 90 days): 15–20%

- Loan book growth over 6 months: 25–30%

All without hiring more underwriters or increasing risk exposure.

Why Custom Credit Engines Beat Off-the-Shelf Scoring APIs

Generic scoring tools offer speed—but not insight. You can't adjust their rules, add new logic, or trust their black-box outcomes.

Invatechs builds scoring engines that match:

- Your industry vertical (invoice finance, SME lending, consumer loans)

- Your regulatory obligations

- Your real-world borrower data (with sandbox testing before live launch)

With your team in control, your tech becomes a strategic advantage, not just another vendor tool.

Ready to Build a Smarter Lending Engine?

Whether you’re a broker platform, embedded lending startup, or licensed lender, Invatechs can help you:

- Automate credit risk analysis

- Reduce manual reviews and delays

- Launch faster, safer, and more competitive offers

Let’s talk about what a modern, AI-powered risk scoring system looks like—for your business.