It's a common point of confusion in the lending world: what's the difference between a Loan Origination System (LOS) and a Loan Management System (LMS)? Many use the terms interchangeably, but they refer to two distinct platforms that handle separate stages of the loan lifecycle. Understanding this difference is key to building an efficient lending operation.

Simply put, a Loan Origination System (LOS) is for getting a new loan on the books. A Loan Management System (LMS) is for servicing the loan once it's been approved and funded.

Let's break it down.

What is a Loan Origination System (LOS)?

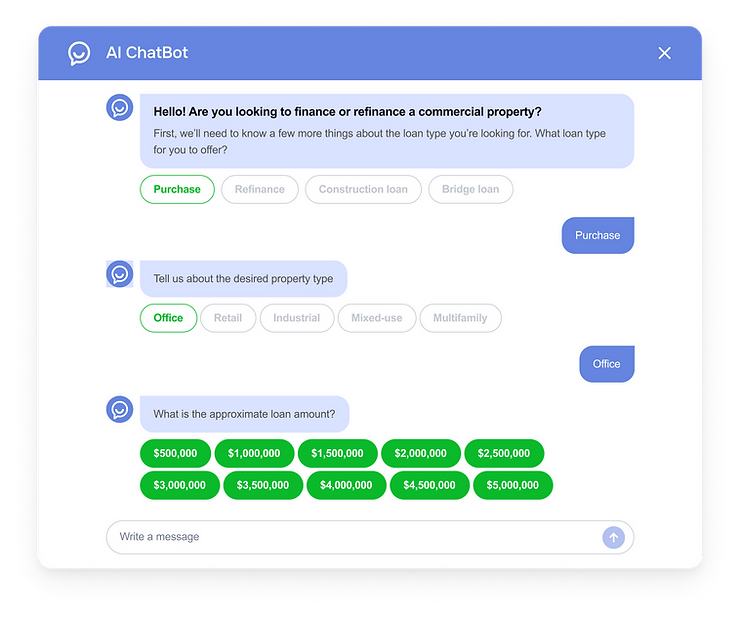

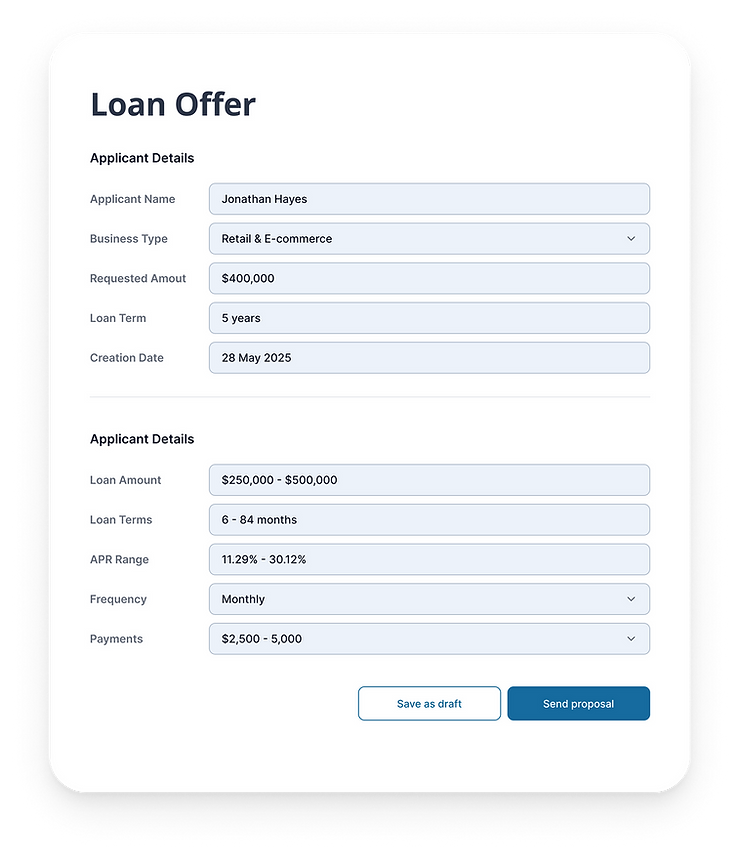

A Loan Origination System, often called loan origination software, is the platform where a new loan application begins its journey. It’s the primary tool for loan officers, underwriters, and processors. Think of it as the "pre-closing" system. The main goal of a LOS is to streamline and automate the complex process of turning an application into an approved loan.

This is the system you need to handle everything from the moment a potential borrower applies until the funds are disbursed. It's the core of any modern lending business, whether you're dealing with mortgages, commercial loans, or business loans.

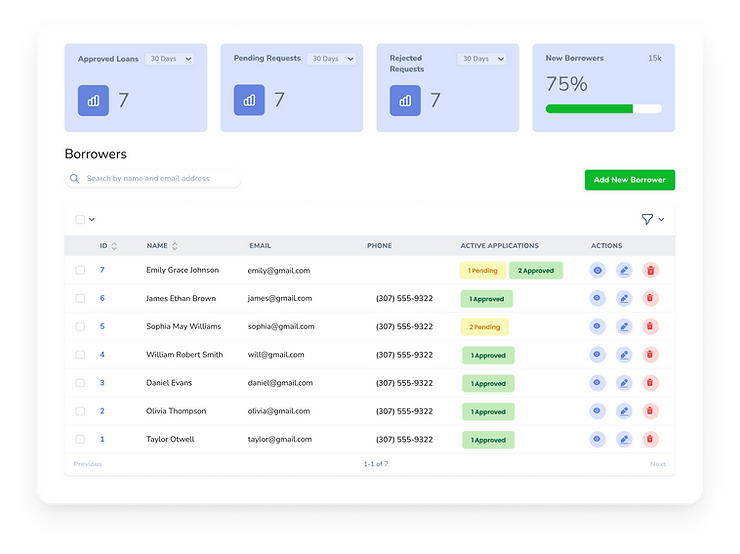

Key functions of an LOS include:

- Application Intake: Capturing borrower information through online portals or direct entry.

- Document Management: Collecting, storing, and verifying required documents like pay stubs, bank statements, and tax returns.

- Credit & Underwriting: Pulling credit reports, running automated underwriting systems (AUS) like Fannie Mae's DU or Freddie Mac's LPA, and providing tools for manual underwriting.

- Compliance Checks: Ensuring the loan application adheres to federal and local regulations (e.g., TILA-RESPA).

- Communication & Collaboration: Acting as a central hub for communication between the borrower, loan officer, processor, and underwriter.

- Closing & Funding: Generating closing documents and coordinating the final steps to fund the loan.

Essentially, the lending origination system is the engine that drives new business. It's a critical piece of mortgage software and commercial loan software for any lender focused on growth.

What is a Loan Management System (LMS)?

Once a loan is originated and funded, the job isn't over. It now needs to be managed for its entire lifespan, which could be months or decades. This is where a Loan Management System (LMS), also known as loan management software or loan servicing software, takes over.

An LMS handles all the "post-closing" activities. Its users are typically loan servicers, accounting departments, and collections teams. The focus of this lending management software is on accuracy, payment processing, and maintaining the loan's health over time.

Key functions of an LMS include:

- Onboarding: Setting up the approved loan from the LOS into the servicing portfolio.

- Payment Processing: Collecting and applying monthly payments (principal, interest, escrow).

- Billing & Statements: Generating and sending regular account statements to borrowers.

- Escrow Management: Managing funds for taxes and insurance and making payments on the borrower's behalf.

- Delinquency & Collections: Tracking late payments, managing collections efforts, and handling modifications or foreclosures if necessary.

- Reporting: Providing detailed reports on portfolio performance, payment histories, and delinquencies.

This business loan software is the backbone of the servicing side of the lending industry, ensuring steady cash flow and proper account management.

The Role of a Mortgage CRM

So where does a customer relationship management system fit in? A mortgage CRM is a glue that connects the entire client journey, often integrating with both the LOS and LMS. While the LOS and LMS are transaction-focused, the CRM is relationship-focused.

A CRM for mortgage brokers or a CRM for mortgage companies manages the relationship from the very first interaction.

- Before Origination: It captures leads, automates marketing, and nurtures potential borrowers until they are ready to apply.

- During Origination: A good CRM system for mortgage brokers integrates with the loan origination system to provide real-time updates to borrowers and real estate agents, reducing manual follow-up.

- After Closing: The CRM doesn't stop. It helps mortgage professionals maintain relationships with past clients, sending them market updates, checking in on their needs, and generating referrals and repeat business.

For any lending institution looking to scale, from a single broker to a large bank offering corporate lending software solutions, a powerful CRM is non-negotiable.

Bringing It All Together

| Feature | Loan Origination System (LOS) | Loan Management System (LMS) |

| Primary Goal | Approve and fund new loans | Service existing loans after funding |

| Stage | Pre-Closing / Origination | Post-Closing / Servicing |

| Primary Users | Loan Officers, Processors, Underwriters | Loan Servicers, Accountants, Collectors |

| Core Tasks | Application, underwriting, document verification, closing | Payment processing, billing, escrow, collections |

| Focus | Speed, efficiency, and compliance in loan approval | Accuracy, automation, and portfolio management |

While some all-in-one platforms claim to do everything, most serious lenders rely on specialised loan software for lenders for each stage. The key is ensuring your LOS, LMS, and mortgage CRM can communicate with each other seamlessly. This integration creates a smooth, efficient workflow from lead generation to loan payoff.

Need a Custom Lending Solution?

Understanding the difference between a LOS and an LMS is the first step. The next is implementing the right technology for your specific needs. Whether you need to build a custom loan origination software from scratch, develop robust commercial lending software, or integrate a powerful CRM for mortgage professionals into your existing workflow, the right tech partner makes all the difference.

At Invatechs, we specialize in developing bespoke software for the financial industry. We build secure, scalable, and intuitive lending software that streamlines operations and drives growth.

Ready to optimize your lending process? Contact Invatechs today for a free consultation and let's build the perfect solution for your business.